| Home | > | Software | > | Tools | > | Effective Interest Rate Model | > | Effective Interest Model Demo |

Effective Interest and Straightline Analysis

Effective Interest Rate Model Page Effective Interest Rate Model Demo

Forfeiture & Expected Life Tool

|

Effective

Interest Model Output and Straight Line Analysis

Once the inputs have been entered, simply click the 'Compute Model' button on the 'Inputs' tab and the model will be computed and written to the 'Model' tab of the workbook. (See Figures 1 and 2).

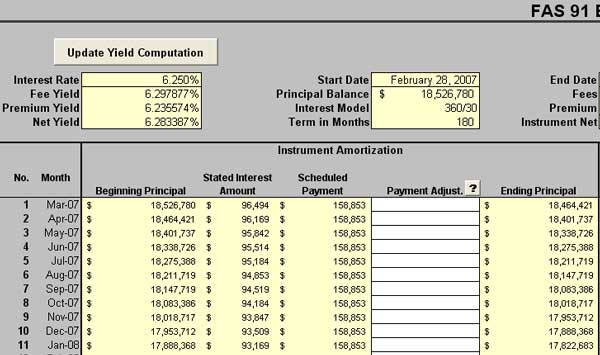

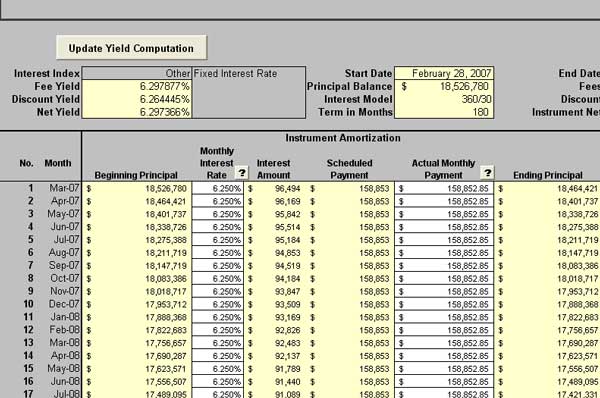

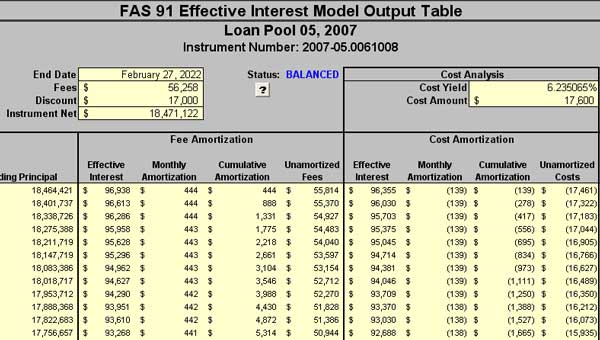

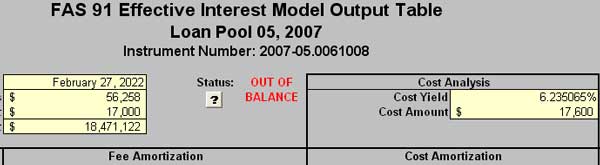

The Fixed Interest model (Figure 2a) considers only a single interest rate over the entire term. Since the interest rate is constant, there is only the need to have adjustments to the scheduled payment in each monthly period. For the Variable Interest rate model (Figure 2b), a monthly interest rate and payment field are provided to adjust for the actual interest rate payment made in each month. The scheduled payment adjusts based on the go-forward interest rate entered for each month but the actual payment made in each period may vary per actual events. In the examples shown in Figure 2, the Yields are computed for the Fees, Costs, Discount/Premium and the Net Yield for the overall instrument. The two models compute Yields using the same method of interpolation for yield values to find an ending amoritization value of 0 for each deferred amount and for the net for the instrument. The result is a level yield for each item. The yields will require update after any payment details change (Payment Adjustment in the Fixed rate model or Actual Monthly Payment in the Variable rate mode). To accomplish this, a button is available labeled 'Update Yield Computation' to re-compute the yields and the Balanced Status indicates BALANCED (see Figure 3a). Whenever changes are made that would cause the Yields to become out of balance, a OUT OF BALANCE warning message appears (see Figure 3b). Anytime the OUT OF BALANCE message appears, simply click the 'Update Yield Computation' button to rebalance the yields.

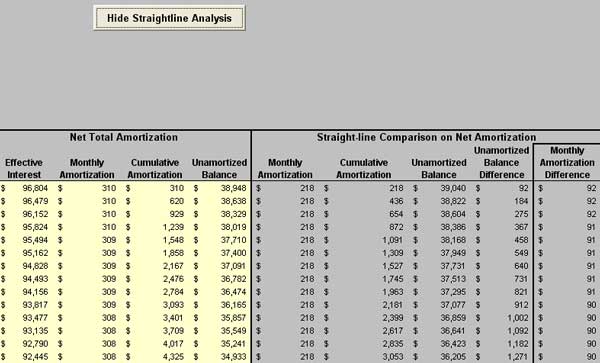

Finally, there are columns that compare the straight-line method used by many companies to compute the monthly amortization costs against the level yield computations. A difference column is provided to show the computed difference between each model. The 'Hide Straightline Analysis' button is provided to reduce page clutter if this information is not required (it will change to 'Show Straightline Analysis' after hiding these rows to allow you to unhide them in the future). (see Figure 4)

The FAS91 Tool provides all of the features you need to track and evaluate your effective interest rates and yields against booked values and can be used to project future amortization as well as provide support for your accounting treatment of these instruments. |

|

Financial Reporting Solutions

©2004,

2005. ProCognis, Inc. All Rights Reserved. Modified

May 24, 2011

Service

Agreement & Privacy Policy